-

PRICES

Monthly Averages

Rallying Gasoil Prices Kept Veg Oil Prices Supported in July

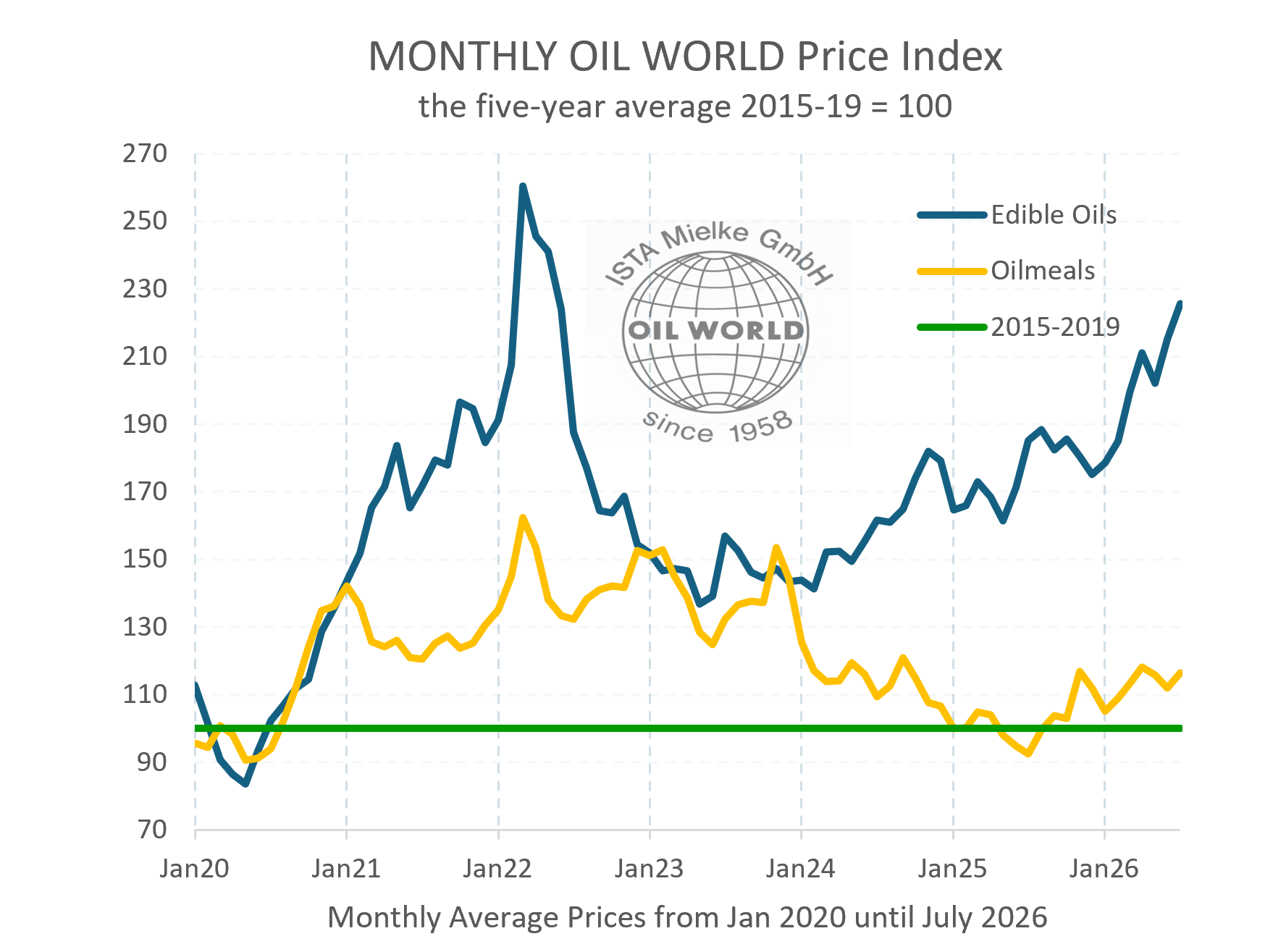

The OIL WORLD Price Index for vegetable oils increased further to 226 points in July, implying that current prices are more than twice as high as the everages in the five years to 2019 .... See the updated monthly average prices for oils & fats until July...

The OIL WORLD Price Index for vegetable oils increased further to 226 points in July, implying that current prices are more than twice as high as the everages in the five years to 2019 .... See the updated monthly average prices for oils & fats until July... -

8 OILS

MONTHLY July 17

World Production Struggling to Keep Up With Demand

Farmers have reacted to price signals and expanded cultivation of oilseeds, primarily with high oil contents. This is setting the stage for large increases in world production of sunflower oil and rapeseed oil next season, probably required urgently if the anticipated declines in world production and exports of palm oil materialize. The magnitude of the latter still depends on several variables like the effects of the current El Niño on the productivity of oil palms in Southeast Asia.

Despite the dynamics unfolding on the seed oil supply side, the growth of world production of eight major vegetable oils is currently forecast to slow down pronouncedly to only about 3.1 Mn T next season. Rising biodiesel production will continue to be a key demand driver for vegetable oils also next season, promoted by admixture targets. The demand for food will rather be determined by market forces...Latest OIL WORLD supply and demand estimates in the MONTHLY...

-

8 OILMEALS

MONTHLY July 17

Rally in Oilmeal Prices Likely to Be Short-lived

Escalating tensions between Russia and Ukraine are currently severely affecting exports of oilseeds & grains from the Black Sea region. Rallying prices of feed grains have also pushed soya meal prices higher ...

However, world supplies are likely to remain ample in 2026/27. In addition to the prospective increase of 6.4 Mn T in world soya meal output, production of 7 other oilmeals seen rising by 3.1 Mn T next season...

-

EU-27

WEEKLY July 3

EU Oilseed Crushings Forecast to Rise by 0.6 Mn T or 1% in 2026/27

Sunflowerseed crushings are seen rebounding in 2026/27 and are forecast to reach a 3-year high of 8.5 Mn T, with biggest gains in Romania, France, Hungary and Bulgaria...

We anticipate rapeseed crushings in the EU to virtually stagnate at around 26.3 Mn T in 2026/27. Imports are set to decline, primarily from Canada and Australia.... Soybean crushings will probably also stagnate next season at the reduced level of 14.9 Mn T likely to be registered in 2025/26....

-

BIODIESEL

WEEKLY June 26

World Biodiesel Production May Increase by 6.7 Mn T in 2026

Biofuels likely to account for 22% of world consumption of oils & fats in 2025/26.

Combined world production of biodiesel and HVO is tentatively estimated at 69.5 Mn T in Jan/Dec 2026. Following a setback by 1.9 Mn T in 2025, production is seen increasing by as much as 6.7 Mn T this year. The reversal of the production trend is occurring primarily in the USA where the delayed release of policy guidelines had resulted in a reduction of biodiesel/HVO production by 2.8 Mn T in 2025. The release of ambitious admixture mandates early this year has triggered a sharp increase and may lift output of biodiesel and HVO in the USA to a new high ....

Usage of 17 oils and fats for biofuel production is seen increasing to an estimated 59.3 Mn T in Oct/Sept 2025/26 (excluding UCO). This raises the share absorbed by the energy market to a new high of 22%. By country estimates in the WEEKLY...

-

ANNUAL 2026

June 2026

Order Your OIL WORLD Annual 2026 NOW

Fundamentals Point to Increasing Vegetable Oil Prices in 2026/27

The stage is set for a bullish price outlook for vegetable oils in the next 12 months. Prospects point to a global production deficit of 17 oils & fats as well as to inevitable demand rationing and higher prices. Our 2026/27 supply & demand forecasts of oilseeds, oils & fats and oilmeals - prepared in early June 2026 - point to tightness developing for oils & fats worldwide and higher prices, rising dependence on seed oils and a resulting further sizable increase in oilseed crushings as well as ample supplies of oilmeals. This will be reflected in deviating price trends, with additional upward momentum for vegetable oils and downward pressure on oilmeals. Seed oils will have to finance an even larger share of the crush margin next season, pushing the oil share even higher. The relative strength of oil & fat prices relative to oilmeals – already ongoing since 2024 - is likely to continue in 2026/27.For producers and consumers alike the global markets will again provide great challenges and opportunities this year. To take advantage of them you require the independent and competent information and forecasts we are providing in this unique compendium.

In the 2026 issue of the OIL WORLD ANNUAL we analyse all the important price-making factors and publish our first 2026/27 projections for each of the 10 oilseeds, 17 oils & fats and 12 oilmeals. The ANNUAL focusses also on demand for vegetable oils and animal fats as a feedstock for biofuel production and its impact on the total global demand, trade and prices of oils and fats as well as the repercussions on oilseeds and oilmeals. This includes world production of biodiesel (with breakdown by country) as well as biodiesel imports and exports of major countries. More details in the just released OIL WORLD Annual 2026....

-

OILSEEDS

WEEKLY June 12

Soybean Crush Up 95 Mn T in 10 Years

Under the lead of soybeans, world oilseed crushings will rise sharply for the third consecutive year to about 580.0 Mn T in Oct/Sept 2025/26, representing an increase of 65 Mn T within three years. The global dependence on soybeans has accelerated since 2023/24, while the growth in other oilseeds fell back, mainly owing to weather-caused production losses in some major sunflowerseed and rapeseed producing regions.

We estimate world crushings of soybeans at 372.3 Mn T in Oct/Sept 2025/26. This is 11.2 Mn T above last season and brings the combined increase within three years to a staggering 56.1 Mn T. The increase has taken place primarily in China as well as in the USA, Brazil and Argentina. In 2015/16, soybean processing amounted to 277 Mn T, implying a significant increase of 95 Mn T within 10 years...

Twitter

Twitter

Hamburg, Germany

--- World Market Prices in US-$/T ---

--- World Market Prices in US-$/T ---

-

- 494 O

- Aug 6

- Soybeans,fob Brazil

-

- 1173 S

- Aug 6

- Palm olein RBD, fob Mal

-

- 600 S

- Aug 6

- Rapeseed, Europe, cif Hamburg

-

- 355 S

- Aug 6

- Soya Meal, fob Arg